Time Series Anomaly Detection¶

Feng Li

School of Statistics and Mathematics

Central University of Finance and Economics

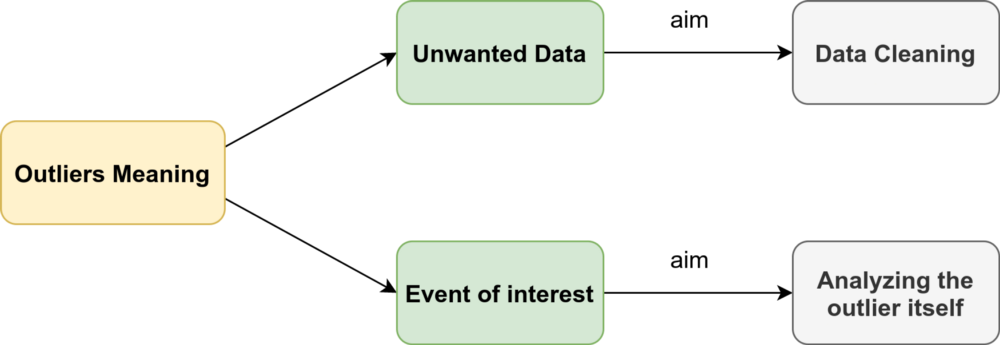

What do outliers mean?¶

Are time series outliers all harmful?¶

Baseline: Whether outliers are noise or useful signal, it purely depends upon business objective.

Business objective - How to retain Premium customers?

Here premium customers can be defined on the basis on their usage (let's consider monthly usage is more then Rs. 5000). Percentage of such customers over total customer base will be very less (let say 3%). So such customer will become outliers as their usages are very much different from the usages (let say Rs. 750) of most of the customers (here 97%). However those outliers are our main data of analysis. So these outliers are good & can't be excluded.

Business objective - To analyse the usage pattern of customers.

If we will include above mentioned premium customers (or a customer whose average monthly usage is Rs. 1000 but one month, it has been Rs. 4000 due to some reason) in analyzing usage pattern of all customers then their effect will be bad on model's outcome. Hence these customer's usages are bad outliers & needs to removed these records.

Business objective - To analyse the fraud in shopping using credit cards.

If a customer never do any purchases in the night however their is an transaction at 2:00 AM. This transaction is a candidate of good outlier as it may be used to detect fraud.

Business objective - To analyse the transaction of sale for the last 1 year for a product (e.g. Bread)

Normally the average units of bread bought in any transaction are 1-8 units. But one week suddenly it has been 10-20 units of bread transaction. On the further investigation it was found that, the people were stocking the bread because they were expecting the storm to hit at that location in that week. If you are interested in looking at sale of bread on regular basis, you may not want to involve a situation which include a storm in your model because it is not a normal behavior. So that weeks' transactions are bad outliers & needs to be removed.

- Example: are you aware of the Gamestop frenzy? A slew of young retail investors bought GME stock to get back at big hedge funds, driving the stock price way up. That sudden, short-lived spike that occurred due to an unlikely event is an additive (point) outlier. The unexpected growth of a time-based value in a short period (looks like a sudden spike) comes under additive outliers.

Subsequence outlier¶

Consecutive points in time whose joint behavior is unusual, although each observation individually is not necessarily a point outlier.

Subsequence outliers can also be global or local, and can affect one (univariate subsequence outlier) or more (multivariate subsequence outlier) time-dependent variables.

Anomaly detection techniques¶

STL decomposition

Classification and Regression Trees (CART)

Clustering-based anomaly detection

Detection using Forecasting

STL decomposition¶

STL stands for seasonal-trend decomposition procedure based on LOESS. This technique gives you the ability to split your time series signal into three parts: seasonal, trend, and residue.

It works for seasonal time-series, which is also the most popular type of time series data. To generate an STL decomposition plot, we just use the ever-amazing

statsmodelsto do the heavy lifting for us.

Anomaly detection using STL decomposition is simple and robust. It can handle a lot of different situations, and all anomalies can still be intuitively interpreted.

The biggest downside of this technique is rigid tweaking options. Apart from the threshold and maybe the confidence interval, there is not much you can do about it.

For example, When you are tracking users on your website that was closed to the public and then was suddenly opened (due to COVID 19). In this case, you should track anomalies that occur before and after launch periods separately.

Anomaly detection with Sales Data¶

import numpy as np

import pandas as pd

from datetime import datetime

def parser(s):

return datetime.strptime(s, '%Y-%m-%d')

catfish_sales = pd.read_csv('data/catfish.csv', parse_dates=[0], index_col=0, date_parser=parser)

#infer the frequency of the data

catfish_sales = catfish_sales.asfreq(pd.infer_freq(catfish_sales.index))

catfish_sales

| Total | |

|---|---|

| Date | |

| 1986-01-01 | 9034 |

| 1986-02-01 | 9596 |

| 1986-03-01 | 10558 |

| 1986-04-01 | 9002 |

| 1986-05-01 | 9239 |

| ... | ... |

| 2012-08-01 | 14442 |

| 2012-09-01 | 13422 |

| 2012-10-01 | 13795 |

| 2012-11-01 | 13352 |

| 2012-12-01 | 12716 |

324 rows × 1 columns

Introducing an anomaly¶

start_date = datetime(1996,1,1)

end_date = datetime(2000,1,1)

lim_catfish_sales = catfish_sales[start_date:end_date]

lim_catfish_sales.loc["1998-12-1"]['Total'] = 10000 # Introduce an anomaly

lim_catfish_sales

| Total | |

|---|---|

| Date | |

| 1996-01-01 | 20322 |

| 1996-02-01 | 20613 |

| 1996-03-01 | 22704 |

| 1996-04-01 | 20276 |

| 1996-05-01 | 20669 |

| 1996-06-01 | 18074 |

| 1996-07-01 | 18719 |

| 1996-08-01 | 20217 |

| 1996-09-01 | 19642 |

| 1996-10-01 | 20842 |

| 1996-11-01 | 18204 |

| 1996-12-01 | 16898 |

| 1997-01-01 | 20746 |

| 1997-02-01 | 23058 |

| 1997-03-01 | 24624 |

| 1997-04-01 | 22154 |

| 1997-05-01 | 22444 |

| 1997-06-01 | 21471 |

| 1997-07-01 | 21866 |

| 1997-08-01 | 22548 |

| 1997-09-01 | 21518 |

| 1997-10-01 | 23408 |

| 1997-11-01 | 19645 |

| 1997-12-01 | 18278 |

| 1998-01-01 | 23576 |

| 1998-02-01 | 26650 |

| 1998-03-01 | 26207 |

| 1998-04-01 | 23195 |

| 1998-05-01 | 22960 |

| 1998-06-01 | 23002 |

| 1998-07-01 | 22973 |

| 1998-08-01 | 24089 |

| 1998-09-01 | 22805 |

| 1998-10-01 | 23241 |

| 1998-11-01 | 21581 |

| 1998-12-01 | 10000 |

| 1999-01-01 | 23107 |

| 1999-02-01 | 25780 |

| 1999-03-01 | 28544 |

| 1999-04-01 | 23488 |

| 1999-05-01 | 23964 |

| 1999-06-01 | 23720 |

| 1999-07-01 | 25069 |

| 1999-08-01 | 24618 |

| 1999-09-01 | 24430 |

| 1999-10-01 | 25229 |

| 1999-11-01 | 22344 |

| 1999-12-01 | 22372 |

| 2000-01-01 | 25412 |

import matplotlib.pyplot as plt

plt.figure(figsize=(10,4))

plt.plot(lim_catfish_sales)

plt.title('Catfish Sales in 1000s of Pounds', fontsize=20)

plt.ylabel('Sales', fontsize=16)

for year in range(start_date.year,end_date.year):

plt.axvline(pd.to_datetime(str(year)+'-01-01'), color='k', linestyle='--', alpha=0.2)

Anomaly detection using STL Decompose¶

from statsmodels.tsa.seasonal import seasonal_decompose

import matplotlib.dates as mdates

plt.rc('figure',figsize=(12,8))

plt.rc('font',size=15)

result = seasonal_decompose(lim_catfish_sales,model='additive')

fig = result.plot()

plt.rc('figure',figsize=(12,6))

plt.rc('font',size=15)

fig, ax = plt.subplots()

x = result.resid.index

y = result.resid.values

ax.plot_date(x, y, color='black',linestyle='--')

ax.annotate('Anomaly', (mdates.date2num(x[35]), y[35]), xytext=(30, 20),

textcoords='offset points', color='red',arrowprops=dict(facecolor='red',arrowstyle='fancy'))

fig.autofmt_xdate()

plt.show()

CART based anomaly detection using isolation forest¶

The main idea is to explicitly identify anomalies instead of profiling normal data points.

In other words, Isolation Forest detects anomalies purely based on the fact that anomalies are data points that are few and different. The anomalies isolation is implemented without employing any distance or density measure.

Isolation Forest is one popular CART method, like any tree ensemble method, is based on decision trees.

When applying an Isolation Forest model, we set

contamination = outliers_fraction, that is telling the model what proportion of outliers are present in the data. This is a trial/error metric.The algorithm fits, predicts (data), and performs outlier detection on data, and returns 1 for normal, -1 for the anomaly.

from sklearn.preprocessing import StandardScaler

from sklearn.decomposition import PCA

from sklearn.covariance import EllipticEnvelope

from sklearn.ensemble import IsolationForest

catfish_sales.loc["1998-12-1"]['Total'] = 10000 # Introduce an anomaly

catfish_sales.loc["1993-3-1"]['Total'] = 30000

catfish_sales.loc["2003-3-1"]['Total'] = 35000

plt.rc('figure',figsize=(12,6))

plt.rc('font',size=15)

catfish_sales.plot()

<AxesSubplot:xlabel='Date'>

scaler = StandardScaler()

np_scaled = scaler.fit_transform(catfish_sales.values.reshape(-1, 1))

data = pd.DataFrame(np_scaled)

# train isolation forest

outliers_fraction = float(0.01)

model = IsolationForest(contamination=outliers_fraction)

model.fit(data)

IsolationForest(contamination=0.01)

catfish_sales['anomaly'] = model.predict(data)

catfish_sales

| Total | anomaly | |

|---|---|---|

| Date | ||

| 1986-01-01 | 9034 | 1 |

| 1986-02-01 | 9596 | 1 |

| 1986-03-01 | 10558 | 1 |

| 1986-04-01 | 9002 | 1 |

| 1986-05-01 | 9239 | 1 |

| ... | ... | ... |

| 2012-08-01 | 14442 | 1 |

| 2012-09-01 | 13422 | 1 |

| 2012-10-01 | 13795 | 1 |

| 2012-11-01 | 13352 | 1 |

| 2012-12-01 | 12716 | 1 |

324 rows × 2 columns

# visualization

fig, ax = plt.subplots(figsize=(10,6))

a = catfish_sales.loc[catfish_sales['anomaly'] == -1, ['Total']] #anomaly

ax.plot(catfish_sales.index, catfish_sales['Total'], color='black', label = 'Normal')

ax.scatter(a.index,a['Total'], color='red', label = 'Anomaly')

plt.legend()

plt.show();

Exercise¶

Re do the above steps and change

outliers_fraction=float(0.01)from0.01to0.05. What could you see?When

outliers_fraction=float(0.05), why there are many outliers detected at the bottom left?

Anomaly detection using clustering method¶

The approach is pretty straightforward. Data instances that fall outside of defined clusters could potentially be marked as anomalies.

Dataset Description: Data contains information on shopping and purchase as well as information on price competitiveness.

df = pd.read_csv('data/TimeSeriesExpedia.csv')

df

| srch_id | date_time | site_id | visitor_location_country_id | visitor_hist_starrating | visitor_hist_adr_usd | prop_country_id | prop_id | prop_starrating | prop_review_score | ... | comp6_rate_percent_diff | comp7_rate | comp7_inv | comp7_rate_percent_diff | comp8_rate | comp8_inv | comp8_rate_percent_diff | click_bool | gross_bookings_usd | booking_bool | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 63 | 2013-05-23 11:56:25 | 14 | 100 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 1 | 90 | 2013-04-23 11:12:24 | 14 | 100 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 2 | 133 | 2013-03-14 11:27:28 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 3 | 148 | 2013-03-21 02:24:03 | 10 | 4 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 4 | 203 | 2013-01-03 20:48:24 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 1.0 | 0.0 | 14.0 | 0 | NaN | 0 |

| 5 | 375 | 2013-01-19 16:51:27 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 6 | 712 | 2013-01-26 11:34:23 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 7 | 751 | 2013-04-29 09:39:50 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 8 | 803 | 2013-03-25 19:43:44 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 9 | 932 | 2013-01-02 22:01:57 | 32 | 220 | 4.00 | 246.15 | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 10 | 979 | 2012-12-17 21:37:18 | 15 | 55 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 11 | 1167 | 2013-01-11 07:46:51 | 14 | 100 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 1.0 | 0.0 | 16.0 | 1 | 270.27 | 1 |

| 12 | 1296 | 2013-05-19 19:52:42 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 13 | 1656 | 2013-06-27 14:49:05 | 15 | 55 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 14 | 1714 | 2012-11-14 17:18:51 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 15 | 1766 | 2013-01-10 19:22:49 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 16 | 1834 | 2013-03-27 14:49:27 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 17 | 1960 | 2013-05-20 08:14:41 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | -1.0 | 6.0 | 0 | NaN | 0 |

| 18 | 2210 | 2013-06-30 08:49:46 | 5 | 77 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 19 | 2327 | 2013-06-27 19:02:34 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 20 | 2426 | 2013-05-21 18:49:33 | 31 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 21 | 2508 | 2012-11-25 18:24:55 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 22 | 2525 | 2013-04-07 22:42:16 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 23 | 2574 | 2013-05-24 21:03:54 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 24 | 2718 | 2013-05-04 08:31:26 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 25 | 2982 | 2013-01-28 21:14:48 | 5 | 187 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 26 | 3000 | 2013-01-25 16:58:42 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 27 | 3249 | 2012-11-02 16:05:35 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 28 | 3700 | 2013-03-01 18:51:53 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 29 | 3898 | 2013-06-15 10:13:01 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 30 | 3944 | 2012-12-09 11:39:06 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 31 | 4016 | 2012-11-18 22:06:17 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 32 | 4210 | 2012-11-01 03:06:43 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 2.0 | 0 | NaN | 0 |

| 33 | 4212 | 2012-11-25 22:29:04 | 32 | 220 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 34 | 4286 | 2013-01-23 18:36:47 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 35 | 4371 | 2013-02-09 20:24:55 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 36 | 4454 | 2013-05-30 16:19:31 | 14 | 100 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 37 | 4508 | 2013-04-16 06:05:58 | 5 | 219 | 3.08 | 37.57 | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 38 | 5086 | 2013-04-24 16:54:51 | 5 | 219 | 3.00 | 135.03 | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 39 | 5110 | 2013-01-09 12:24:36 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 16.0 | 1 | 633.92 | 1 |

| 40 | 5223 | 2013-05-08 13:46:34 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 1 | NaN | 0 |

| 41 | 5518 | 2012-11-05 21:05:35 | 14 | 100 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 42 | 5724 | 2013-05-02 18:20:27 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 43 | 5859 | 2012-12-31 11:13:27 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 44 | 5887 | 2013-03-29 23:14:12 | 5 | 123 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 45 | 5927 | 2013-05-17 17:25:15 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 46 | 5972 | 2012-12-18 07:56:34 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 47 | 6085 | 2012-12-20 08:37:44 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 48 | 6281 | 2013-05-08 22:15:41 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 49 | 6290 | 2013-01-24 22:08:31 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 6.0 | 0 | NaN | 0 |

| 50 | 6299 | 2013-05-20 10:25:55 | 14 | 100 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 51 | 6363 | 2012-12-27 11:21:45 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

| 52 | 6551 | 2013-05-12 06:11:34 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0 | NaN | 0 |

| 53 | 6681 | 2013-02-28 15:19:54 | 5 | 219 | NaN | NaN | 219 | 104517 | 4 | 4.0 | ... | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | 0 | NaN | 0 |

54 rows × 54 columns

Detecting the number of clusters

- First we need to know the number of clusters.

- The Elbow Method works pretty efficiently for this.

- The Elbow method is a graph of the number of clusters vs the variance explained/objective/score

from sklearn.cluster import KMeans

data = df[['price_usd', 'srch_booking_window', 'srch_saturday_night_bool']]

n_cluster = range(1, 20)

kmeans = [KMeans(n_clusters=i).fit(data) for i in n_cluster]

scores = [kmeans[i].score(data) for i in range(len(kmeans))]

fig, ax = plt.subplots(figsize=(10,6))

ax.plot(n_cluster, scores)

plt.xlabel('Number of Clusters')

plt.ylabel('Score')

plt.title('Elbow Curve')

plt.show();

From the above elbow curve, we see that the graph levels off after 10 clusters, implying that the addition of more clusters do not explain much more of the variance in our relevant variable; in this case

price_usd.We set

n_clusters=10, and upon generating the k-means output, use the data to plot the 3D clusters.

X = df[['price_usd', 'srch_booking_window', 'srch_saturday_night_bool']]

X = X.reset_index(drop=True)

km = KMeans(n_clusters=10)

km.fit(X)

km.predict(X)

labels = km.labels_

# #Plotting

from mpl_toolkits.mplot3d import Axes3D

fig,ax = plt.subplots(figsize=(10,6))

ax = Axes3D(fig, rect=[0, 0, 0.95, 1], elev=48, azim=134, auto_add_to_figure=False)

fig.add_axes(ax)

ax.scatter(X.iloc[:,0], X.iloc[:,1], X.iloc[:,2],

c=labels.astype(np.float), edgecolor="k")

ax.set_xlabel("price_usd")

ax.set_ylabel("srch_booking_window")

ax.set_zlabel("srch_saturday_night_bool")

plt.title("K Means", fontsize=14);

We see that the first component explains almost 50% of the variance. The second component explains over 30%. However, notice that almost none of the components are really negligible. The first 2 components contain over 80% of the information. So, we will set

n_components=2.The underlying assumption in the clustering-based anomaly detection is that if we cluster the data, normal data will belong to clusters while anomalies will not belong to any clusters, or belong to small clusters.

data = df[['price_usd', 'srch_booking_window', 'srch_saturday_night_bool']]

X = data.values

X_std = StandardScaler().fit_transform(X)

#Calculating Eigenvecors and eigenvalues of Covariance matrix

mean_vec = np.mean(X_std, axis=0)

cov_mat = np.cov(X_std.T)

eig_vals, eig_vecs = np.linalg.eig(cov_mat)

# Create a list of (eigenvalue, eigenvector) tuples

eig_pairs = [ (np.abs(eig_vals[i]),eig_vecs[:,i]) for i in range(len(eig_vals))]

eig_pairs.sort(key = lambda x: x[0], reverse= True)

# Calculation of Explained Variance from the eigenvalues

tot = sum(eig_vals)

var_exp = [(i/tot)*100 for i in sorted(eig_vals, reverse=True)] # Individual explained variance

cum_var_exp = np.cumsum(var_exp) # Cumulative explained variance

plt.figure(figsize=(10, 5))

plt.bar(range(len(var_exp)), var_exp, alpha=0.3, align='center', label='individual explained variance', color = 'y')

plt.step(range(len(cum_var_exp)), cum_var_exp, where='mid',label='cumulative explained variance')

plt.ylabel('Explained variance ratio')

plt.xlabel('Principal components')

plt.legend(loc='best')

plt.show();

# Take useful feature and standardize them

data = df[['price_usd', 'srch_booking_window', 'srch_saturday_night_bool']]

X_std = StandardScaler().fit_transform(X)

data = pd.DataFrame(X_std)

# reduce to 2 important features

pca = PCA(n_components=2)

data = pca.fit_transform(data)

# standardize these 2 new features

scaler = StandardScaler()

np_scaled = scaler.fit_transform(data)

data = pd.DataFrame(np_scaled)

kmeans = [KMeans(n_clusters=i).fit(data) for i in n_cluster]

df['cluster'] = kmeans[9].predict(data)

df.index = data.index

df['principal_feature1'] = data[0]

df['principal_feature2'] = data[1]

df['cluster'].value_counts()

3 14 8 10 0 8 7 4 1 4 2 4 6 3 5 3 4 2 9 2 Name: cluster, dtype: int64

- Calculate the distance between each point and its nearest centroid. The biggest distances are considered anomalies.

We use

outliers_fractionto provide information to the algorithm about the proportion of the outliers present in our data set.Similarly to the IsolationForest algorithm. This is largely a hyperparameter that needs hit/trial or grid-search to be set right – as a starting figure, let’s estimate,

outliers_fraction=0.1

# return Series of distance between each point and its distance with the closest centroid

def getDistanceByPoint(data, model):

distance = pd.Series(dtype='float64')

for i in range(0,len(data)):

Xa = np.array(data.loc[i])

Xb = model.cluster_centers_[model.labels_[i]-1]

distance.at[i]=np.linalg.norm(Xa-Xb)

return distance

outliers_fraction = 0.1

# get the distance between each point and its nearest centroid. The biggest distances are considered as anomaly

distance = getDistanceByPoint(data, kmeans[9])

number_of_outliers = int(outliers_fraction*len(distance))

threshold = distance.nlargest(number_of_outliers).min()

# anomaly1 contain the anomaly result of the above method Cluster (0:normal, 1:anomaly)

df['anomaly1'] = (distance >= threshold).astype(int)

fig, ax = plt.subplots(figsize=(10,6))

colors = {0:'blue', 1:'red'}

ax.scatter(df['principal_feature1'], df['principal_feature2'], c=df["anomaly1"].apply(lambda x: colors[x]))

plt.xlabel('principal feature1')

plt.ylabel('principal feature2')

plt.show();

df = df.sort_values('date_time')

#df['date_time_int'] = df.date_time.astype(np.int64)

fig, ax = plt.subplots(figsize=(10,6))

a = df.loc[df['anomaly1'] == 1, ['date_time', 'price_usd']] #anomaly

ax.plot(pd.to_datetime(df['date_time']), df['price_usd'], color='k',label='Normal')

ax.scatter(pd.to_datetime(a['date_time']),a['price_usd'], color='red', label='Anomaly')

ax.xaxis_date()

plt.xlabel('Date Time')

plt.ylabel('price in USD')

plt.legend()

fig.autofmt_xdate()

plt.show()

Anomaly detection using Forecasting¶

Several points from the past generate a forecast of the next point with the addition of some random variable, which is usually white noise.

Forecasted points in the future will generate new points and so on. Its obvious effect on the forecast horizon – the signal gets smoother.

Each time you work with a new signal, you should build a new forecasting model.

Your signal should be stationary after differencing. In simple words, it means your signal should not be dependent on time, which is a significant constraint.

We can utilize different forecasting methods such as Moving Averages, Autoregressive approach, and ARIMA with its different variants.

The difficult part of using this method is that you should select the number of differences, number of autoregressions, and forecast error coefficients.

The procedure for detecting anomalies with ARIMA is:

Predict the new point from past datums and find the difference in magnitude with those in the training data.

Choose a threshold and identify anomalies based on that difference threshold.

We use a popular module in time series called

prophet. This module specifically caters to stationarity and seasonality, and can be tuned with some hyper-parameters.

t = pd.DataFrame()

t['ds'] = catfish_sales.index

t['y'] = catfish_sales['Total'].values

t

| ds | y | |

|---|---|---|

| 0 | 1986-01-01 | 9034 |

| 1 | 1986-02-01 | 9596 |

| 2 | 1986-03-01 | 10558 |

| 3 | 1986-04-01 | 9002 |

| 4 | 1986-05-01 | 9239 |

| ... | ... | ... |

| 319 | 2012-08-01 | 14442 |

| 320 | 2012-09-01 | 13422 |

| 321 | 2012-10-01 | 13795 |

| 322 | 2012-11-01 | 13352 |

| 323 | 2012-12-01 | 12716 |

324 rows × 2 columns

from prophet import Prophet

def fit_predict_model(dataframe, interval_width = 0.99, changepoint_range = 0.8):

m = Prophet(daily_seasonality = False, yearly_seasonality = False, weekly_seasonality = False,

seasonality_mode = 'additive',

interval_width = interval_width,

changepoint_range = changepoint_range)

m = m.fit(dataframe)

forecast = m.predict(dataframe)

forecast['fact'] = dataframe['y'].reset_index(drop = True)

return forecast

pred = fit_predict_model(t)

Initial log joint probability = -15.2405

Iter log prob ||dx|| ||grad|| alpha alpha0 # evals Notes

90 697.457 0.00195447 191.233 1.882e-05 0.001 160 LS failed, Hessian reset

99 698.836 0.0012588 84.3828 0.2852 0.2852 170

Iter log prob ||dx|| ||grad|| alpha alpha0 # evals Notes

195 699.445 0.000884218 84.4718 1.121e-05 0.001 359 LS failed, Hessian reset

199 699.485 0.000215781 52.8067 1 1 363

Iter log prob ||dx|| ||grad|| alpha alpha0 # evals Notes

250 699.636 2.05622e-05 68.2599 3.669e-07 0.001 469 LS failed, Hessian reset

299 699.638 6.66519e-06 61.6449 1 1 537

Iter log prob ||dx|| ||grad|| alpha alpha0 # evals Notes

330 699.638 1.00984e-07 45.3758 1.725e-09 0.001 616 LS failed, Hessian reset

333 699.638 6.38716e-08 41.6343 1 1 619

Optimization terminated normally:

Convergence detected: relative gradient magnitude is below tolerance

def detect_anomalies(forecast):

forecasted = forecast[['ds','trend', 'yhat', 'yhat_lower', 'yhat_upper', 'fact']].copy()

forecasted['anomaly'] = 0

forecasted.loc[forecasted['fact'] > forecasted['yhat_upper'], 'anomaly'] = 1

forecasted.loc[forecasted['fact'] < forecasted['yhat_lower'], 'anomaly'] = -1

#anomaly importances

forecasted['importance'] = 0

forecasted.loc[forecasted['anomaly'] ==1, 'importance'] = \

(forecasted['fact'] - forecasted['yhat_upper'])/forecast['fact']

forecasted.loc[forecasted['anomaly'] ==-1, 'importance'] = \

(forecasted['yhat_lower'] - forecasted['fact'])/forecast['fact']

return forecasted

pred = detect_anomalies(pred)

import altair as alt

def plot_anomalies(forecasted):

interval = alt.Chart(forecasted).mark_area(interpolate="basis", color = '#7FC97F').encode(

x=alt.X('ds:T', title ='date'),

y='yhat_upper',

y2='yhat_lower',

tooltip=['ds', 'fact', 'yhat_lower', 'yhat_upper']

).interactive().properties(

title='Anomaly Detection'

)

fact = alt.Chart(forecasted[forecasted.anomaly==0]).mark_circle(size=15, opacity=0.7, color = 'Black').encode(

x='ds:T',

y=alt.Y('fact', title='Sales'),

tooltip=['ds', 'fact', 'yhat_lower', 'yhat_upper']

).interactive()

anomalies = alt.Chart(forecasted[forecasted.anomaly!=0]).mark_circle(size=30, color = 'Red').encode(

x='ds:T',

y=alt.Y('fact', title='Sales'),

tooltip=['ds', 'fact', 'yhat_lower', 'yhat_upper'],

size = alt.Size( 'importance', legend=None)

).interactive()

return alt.layer(interval, fact, anomalies)\

.properties(width=870, height=450)\

.configure_title(fontSize=20)

plot_anomalies(pred)

How to deal with the anomalies?¶

Understanding the business case¶

Anomalies almost always provide new information and perspective to your problems.

Stock prices going up suddenly? There has to be a reason for this like we saw with Gamestop, a pandemic could be another. So, understanding the reasons behind the spike can help you solve the problem in an efficient manner.

Understanding the business use case can also help you identify the problem better. For instance, you might be working on some sort of fraud detection which means your primary goal is indeed understanding the outliers in the data.

If none of this is your concern, you can move to remove or smoothen out the outlier.