Forecast Reconciliation¶

Feng Li¶

Guanghua School of Management¶

Peking University¶

feng.li@gsm.pku.edu.cn¶

Course home page: https://feng.li/bdcf¶

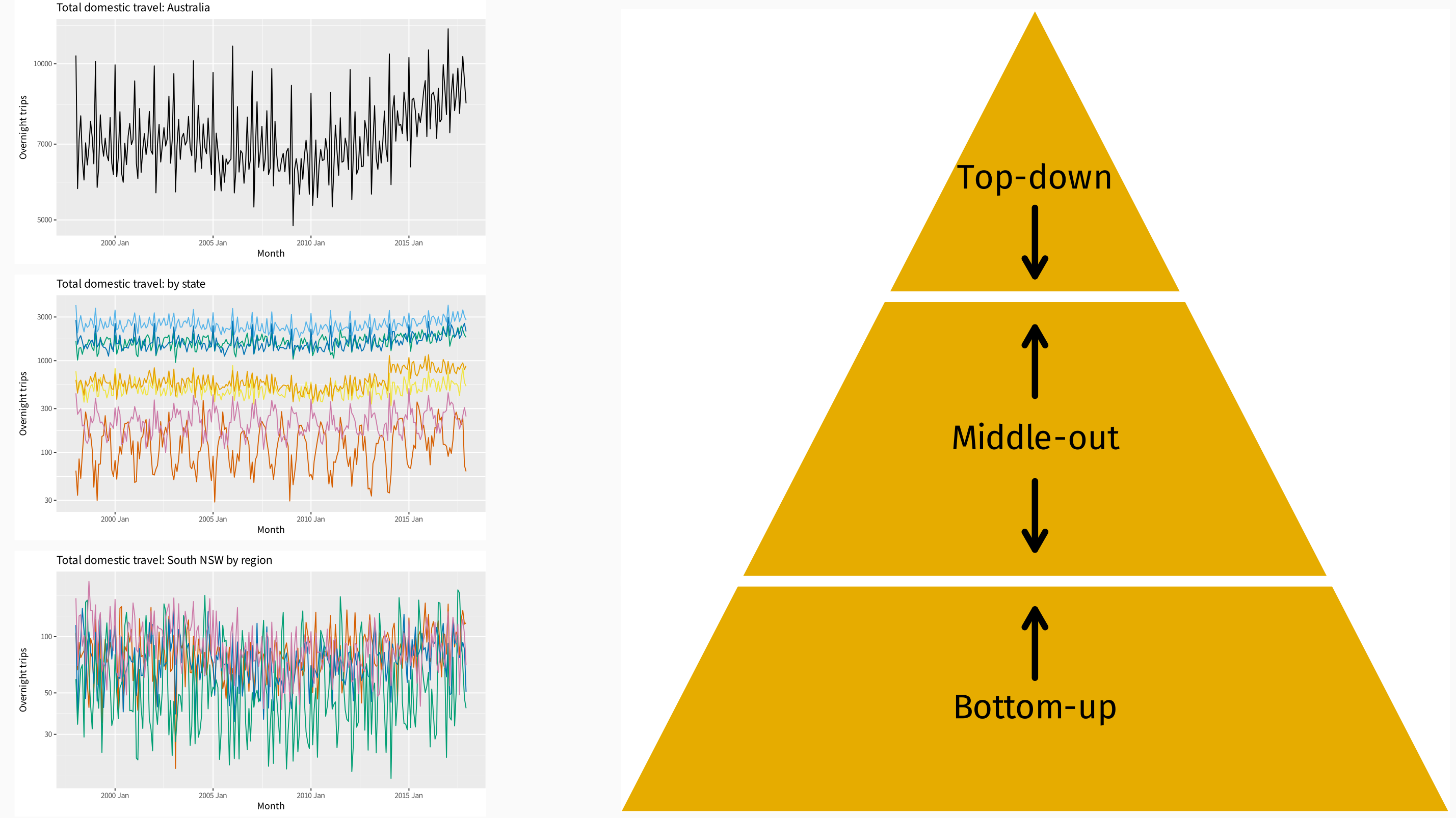

The hierarchical forecasting problem¶

- We want forecasts at all levels of aggregation.

- If we model and forecast each series independently, the forecasts will almost certainly not add up.

- We need to impose constraints on the forecasts to ensure they are "coherent".

- We need to do this in a way that is computationally efficient.

Top-down forecasting¶

- Works well in presence of low counts.

- Single forecasting model easy to build

- Provides reliable forecasts for aggregate levels.

- Loss of information, especially individual series dynamics.

- Distribution of forecasts to lower levels can be difficult

- No prediction intervals

Bottom-up forecasting¶

- No loss of information.

- Better captures dynamics of individual series.

- Large number of series to be forecast.

- Constructing forecasting models is harder because of noisy data at bottom level.

- No prediction intervals

Forecasting notation¶

Let $\hat{\mathbf{y}}_{T+h|T}$ be vector of initial $h$-step forecasts, made at time $T$, stacked in same order as $\mathbf{y}_t$. (In general, they will not "add up".)

Coherent linear forecasts are of the form:

$$ \tilde{\mathbf{y}}_{T+h|T}=\mathbf{S}\mathbf{G}\hat{\mathbf{y}}_{T+h|T} $$

for some matrix $\mathbf{G}$.

- $\mathbf{G}$ extracts and combines base forecasts $\hat{\mathbf{y}}_{T+h|T}$ to get bottom-level forecasts.

- $\mathbf{S}$ adds them up

Single-level methods¶

Bottom-up forecasts are obtained using $$ \mathbf{G} = \left[\mathbf{0}\mid \mathbf{I}\right], $$ where $\mathbf{0}$ is null matrix and $\mathbf{I}$ is identity matrix.

- $\mathbf{G}$ matrix extracts only bottom-level forecasts from $\hat{\mathbf{y}}_{T+h|T}$

- $\mathbf{S}$ adds them up to give the bottom-up forecasts.

Top-down forecasts are obtained using $$ \mathbf{G}= \left[\mathbf{p}\mid\mathbf{0}\right] $$ where $\mathbf{p}=[p_{1},p_{2},\dots,p_{n_b}]'$ and $\sum_{k=1}^{n_b} p_k = 1$.

- $\mathbf{G}$ distributes forecasts of aggregate to lowest level series.

- Different methods of top-down forecasting lead to different proportionality vectors $\mathbf{p}$.

Mean Property of single-level methods¶

$$ \mathbb{E}[\tilde{\mathbf{y}}_{T+h \mid T} \mid \mathbf{y}_1, \ldots, \mathbf{y}_T] = \mathbf{SGE}[\hat{\mathbf{y}}_{T+h \mid T} \mid \mathbf{y}_1, \ldots, \mathbf{y}_T] = \mathbf{SE}[\mathbf{b}_{T+h \mid T} \mid \mathbf{y}_1, \ldots, \mathbf{y}_T] $$

provided $ \mathbf{SGS} = \mathbf{S} $ and

$$ \mathbb{E}[\hat{\mathbf{y}}_{T+h \mid T} \mid \mathbf{y}_1, \ldots, \mathbf{y}_T] = \mathbf{SE}[\mathbf{b}_{T+h \mid T} \mid \mathbf{y}_1, \ldots, \mathbf{y}_T]. $$

Forecasts $ \tilde{\mathbf{y}}_{T+h \mid T} $ are unbiased iff base forecasts $ \hat{\mathbf{y}}_{T+h \mid T} $ are unbiased and $ \mathbf{SGS} = \mathbf{S} $.

$ \mathbf{SGS} = \mathbf{S} $ for bottom-up method

$ \mathbf{SGS} \ne \mathbf{S} $ for top-down method

Variance Property of single-level methods¶

$$ V_h = \mathrm{Var}[\mathbf{y}_{T+h} - \tilde{\mathbf{y}}_{T+h \mid T} \mid \mathbf{y}_1, \ldots, \mathbf{y}_T] = \mathbf{SGW}_h \mathbf{G}^\prime \mathbf{S}^\prime $$

where $\mathbf{W}_h = \mathrm{Var}[\mathbf{y}_{T+h} - \hat{\mathbf{y}}_{T+h \mid T} \mid \mathbf{y}_1, \ldots, \mathbf{y}_T]$

- $\mathbf{W}_h$ is hard to estimate for $h > 1$.

- This suggests we should choose $\mathbf{G}$ to minimise $V_h$.

Minimum trace reconciliation (MinT)¶

If $\mathbf{SG}$ is a projection, then the trace of $V_h$ is minimized when

$$ \mathbf{G} = (\mathbf{S}'\mathbf{W}_h^{-1}\mathbf{S})^{-1} \mathbf{S}' \mathbf{W}_h^{-1} $$

$$ \tilde{\mathbf{y}}_{T+h \mid T} = \mathbf{S}(\mathbf{S}' \mathbf{W}_h^{-1} \mathbf{S})^{-1} \mathbf{S}' \mathbf{W}_h^{-1} \hat{\mathbf{y}}_{T+h \mid T} $$

- Trace of $V_h$ is sum of forecast variances.

- MinT solution is $L_2$ optimal amongst linear unbiased forecasts.

- How to estimate $\mathbf{W}_h = \mathrm{Var}[\mathbf{y}_{T+h} - \hat{\mathbf{y}}_{T+h \mid T} \mid \mathbf{y}_1, \ldots, \mathbf{y}_T]$?

Reconciliation method $G$¶

| Reconciliation method | $G$ |

|---|---|

| OLS | $(\mathbf{S}'\mathbf{S})^{-1}\mathbf{S}'$ |

| WLS(var) | $(\mathbf{S}'\boldsymbol{\Lambda}_s \mathbf{S})^{-1}\mathbf{S}' \boldsymbol{\Lambda}_v$ |

| WLS(struct) | $(\mathbf{S}'\boldsymbol{\Lambda}_s \mathbf{S})^{-1}\mathbf{S}' \boldsymbol{\Lambda}_s$ |

| MinT(sample) | $(\mathbf{S}'\hat{\mathbf{W}}_{\text{sam}}^{-1} \mathbf{S})^{-1} \mathbf{S}' \hat{\mathbf{W}}_{\text{sam}}^{-1}$ |

| MinT(shrink) | $(\mathbf{S}'\hat{\mathbf{W}}_{\text{shr}}^{-1} \mathbf{S})^{-1} \mathbf{S}' \hat{\mathbf{W}}_{\text{shr}}^{-1}$ |

These approximate MinT by assuming $\mathbf{W}_h = k_h \mathbf{W}_1$

- $\boldsymbol{\Lambda}_s = \mathrm{diag}(\mathbf{W}_1)^{-1}$

- $\boldsymbol{\Lambda}_s = \mathrm{diag}(\mathbf{S} \mathbf{1})^{-1}$

- $\hat{\mathbf{W}}_{\text{sam}}$ is sample estimate of the residual covariance matrix

- $\hat{\mathbf{W}}_{\text{shr}}$ is shrinkage estimator

$$ \tau \cdot \mathrm{diag}(\hat{\mathbf{W}}_{\text{sam}}) + (1 - \tau) \hat{\mathbf{W}}_{\text{sam}} $$ where $\tau$ is selected optimally. - Still need a good estimate of $\mathbf{W}_h$ for forecast variance.

Further Reading¶

Gross, C. W., & Sohl, J. E. (1990). Disaggregation methods to expedite product line forecasting. Journal of Forecasting, 9, 233–254. DOI: https://doi.org/10.1002/for.3980090304 provide a good introduction to the top-down approaches.

Athanasopoulos, G., Gamakumara, P., Panagiotelis, A., Hyndman, R.J., Affan, M. (2020). Hierarchical Forecasting. In: Fuleky, P. (eds) Macroeconomic Forecasting in the Era of Big Data. Advanced Studies in Theoretical and Applied Econometrics, vol 52. Springer, Cham. DOI: https://doi.org/10.1007/978-3-030-31150-6_21

Wickramasuriya, S. L., Athanasopoulos, G., & Hyndman, R. J. (2019). Optimal forecast reconciliation for hierarchical and grouped time series through trace minimization. Journal of the American Statistical Association, 114(526), 804–819. DOI: https://doi.org/10.1080/01621459.2018.1448825